Will medical debt ruin my credit score 2026? Understand your options

Empathy Hook

Medical debt can feel like a weight that won’t lift, especially when you’re worried about what it might do to your credit score. You’re not alone in this concern, and you’re not powerless.

Understanding how medical debt affects your credit—and what steps you can take now—can help you protect your financial future while managing what you owe.

Cost Reality Check

Medical debt doesn’t automatically destroy your credit score, but the timeline and reporting practices matter. What stood out was how many people don’t realize they have more control over the process than they think.

📉 The “Under $500” Rule (Key for 2026)

Recent regulations have changed the game for medical debt reporting. Here is what you need to know:

- ✅ Under $500 is Safe: Paid OR unpaid medical collections under $500 should not appear on your credit report.

- ⏳ 1-Year Grace Period: Unpaid medical debt typically cannot be reported to credit bureaus until it is at least 365 days past due. This gives you time to negotiate.

- 🎉 Paid = Deleted: Unlike credit card debt, once you pay off a medical collection (even partially, if agreed), it must be removed completely from your credit report.

The key is acting before unpaid bills move to collections or get reported to credit bureaus. Once you understand the system, you can work within it to minimize damage.

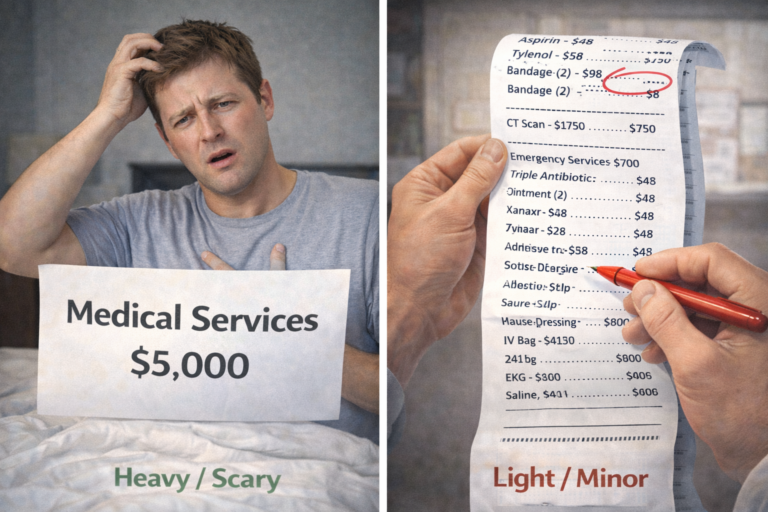

What to Do Right Now

Start by reviewing every medical bill and Explanation of Benefits you’ve received. Check for errors in service dates, charges, and insurance adjustments—mistakes happen more often than you’d expect.

🛡️ 3 Steps to Protect Your Score

-

📞 Step 1: The “Pause” Call

Call the provider’s billing department immediately. Ask: “Can you put my account on hold while I review these charges?” This stops the clock on collections. -

🔍 Step 2: The Itemized Audit

Request an itemized bill. Compare it with your insurance EOB. If insurance denied a claim, appeal it before paying a cent. -

🤝 Step 3: The Negotiation

Ask for “Charity Care” or a “0% Interest Payment Plan.” As long as you are on a payment plan and paying on time, they generally will not send you to collections.

🏥 Strategy Showdown

How different options affect your wallet & credit

Where to Go

For help managing medical debt and understanding your rights, start with your healthcare provider’s financial counseling office. Many hospitals and clinics have staff dedicated to helping patients navigate bills and payment options.

Non-profit credit counseling agencies (look for NFCC accredited) can provide free or low-cost guidance on debt management without the pressure of for-profit debt settlement companies.

💬 Common Questions (FAQ)

Will paying off a collection raise my score?

Yes! For medical debt specifically, the credit bureaus (Equifax, Experian, TransUnion) will delete the collection account from your report once it is paid in full.

Can I be sued for medical debt?

Yes, if the debt is significant and ignored for a long time, providers or collection agencies can sue to garnish wages. This is why communication is key.

Navigator Alex Tip

Before agreeing to any payment plan, ask this exact question: “What is the minimum monthly payment you can accept without sending this account to collections or reporting it to credit bureaus?” This gives you a clear baseline and shows you’re serious about resolving the debt responsibly.

Document the answer in writing, either through email confirmation or a follow-up letter. This creates a paper trail that protects you if disputes arise later.

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Regulations regarding medical debt reporting (like the No Surprises Act and CFPB rules) change frequently. It is not a substitute for professional consultation with a certified credit counselor, financial advisor, or attorney.