The 2026 Insurance Marketplace: A Risk-Hedging Protocol for the Self-Employed

The “Obamacare” Brand is Gone. The Architecture Remains.

Let’s address a persistent misconception. Many assume the Affordable Care Act (ACA) was dismantled. It was not. It was rebranded and bureaucratized.

For W-2 employees with employer-sponsored coverage, this is operationally irrelevant. For 1099 independent contractors or entrepreneurs, the “Marketplace” (formerly branded as Obamacare) represents the singular institutional infrastructure standing between your net worth and a catastrophic medical event.

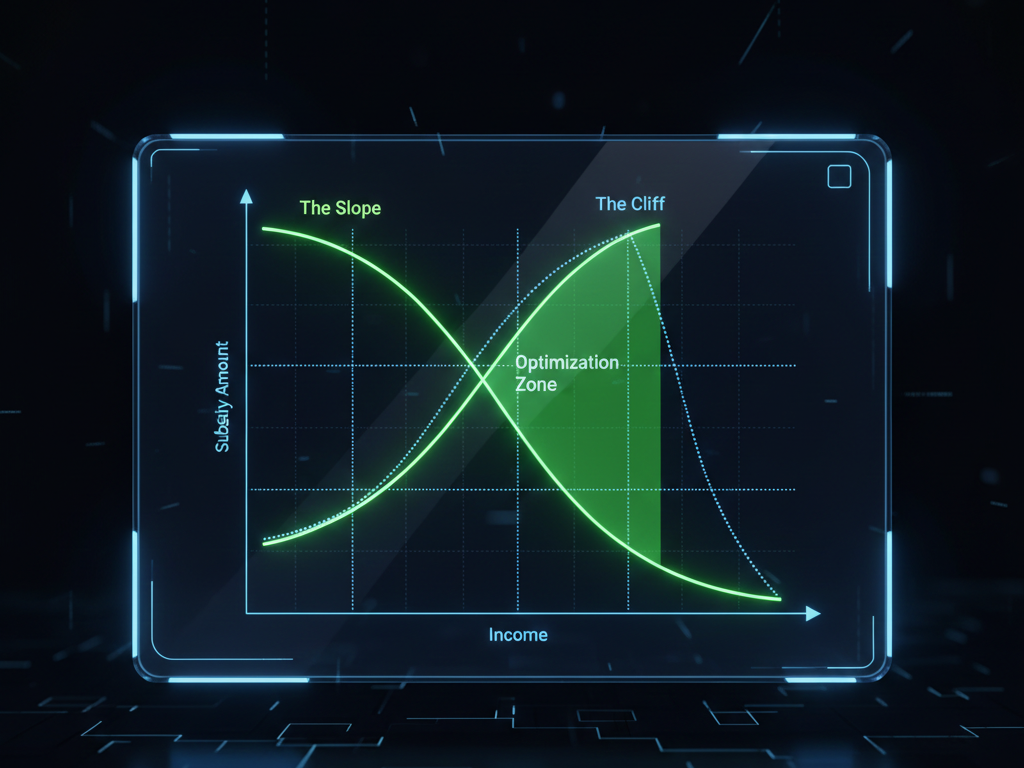

However, the rules of engagement for 2026 have shifted. The “Subsidy Cliff” (where earning $1 above the threshold disqualified you from all assistance) has been replaced by a “Subsidy Slope.” This means your Modified Adjusted Gross Income (MAGI) is now the most critical variable in your financial architecture.

What follows is the strategic framework for navigating the 2026 Marketplace.

Strategic Variable 1: MAGI Engineering

Most individuals apply for insurance coverage after filing their tax returns. This is a tactical error.

The Advanced Premium Tax Credit (APTC)—the federal subsidy that funds your premium payments—is calculated based on your projected income for 2026, not historical earnings.

As of February 2026, coinciding with REAL ID enforcement and updated IRS verification protocols, Marketplace platforms now require additional identity documentation during enrollment, though MAGI projection methodology remains unchanged.

The Strategic Approach: You must forecast your annual income to position yourself within the optimal subsidy band (typically 100% to 400% of the Federal Poverty Level). Overestimation results in providing the government an interest-free loan. Underestimation triggers a substantial “Tax Clawback” liability the following April.

Navigator Protocol: If your income exhibits volatility, bias toward conservative overestimation. Receiving a tax refund is mathematically superior to writing a $2,000 clawback check to the IRS.

Strategic Variable 2: The “Short-Term” Insurance Trap

Execute a search for “Health Insurance” on any major search engine, and you’ll encounter extensive advertising for “Short-Term Health Plans” with premiums as low as $99/month.

Do not engage with these products.

While technically classified as insurance, they’re functionally inadequate. They are not ACA-compliant, meaning they maintain legal authority to deny coverage for “pre-existing conditions.” 2026 claims data demonstrates that 45% of claims submitted to these plans are denied.

The Identification Protocol: If a plan requires medical history disclosure (e.g., “Have you received treatment for diabetes?”), it is NOT a Marketplace-compliant plan. It represents a liability exposure. Authentic Marketplace plans (ACA) never require health history disclosure during enrollment.

Strategic Variable 3: The Silver Tier CSR Arbitrage

When selecting a metal tier (Bronze, Silver, Gold, Platinum), most low-utilization individuals default to Bronze to minimize premium expenditure. This is frequently a miscalculation.

Due to a regulatory mechanism termed “Cost-Sharing Reductions (CSR),” Silver plans are the only tier where federal subsidies apply to your deductible and out-of-pocket maximums, not merely your premium.

The Economic Comparison:

- Bronze Tier: $0 Premium, $9,000 Deductible. (Catastrophic asset protection only)

- Silver Tier (with CSR): $100 Premium, $800 Deductible. (Functional coverage)

If your income falls below 250% of the Federal Poverty Level, Silver plans create an arbitrage opportunity where you receive Gold-equivalent benefits at Silver-tier pricing. Always audit Silver CSR eligibility before defaulting to Bronze.

If determining optimal tier selection and subsidy eligibility feels complex, consider using Marketplace navigation tools that model different income scenarios. (I’ll be analyzing the top 3 ACA Marketplace Calculator Tools for 2026 in my next breakdown.)

Insurance is not healthcare. It is wealth protection. — Alex

⚠️ Operational Disclaimer

I function as a strategic navigator analyzing insurance market mechanisms—not as a licensed insurance broker or tax professional. The strategies outlined (MAGI Engineering, CSR Arbitrage) are based on 2026 federal ACA guidelines and may exhibit variance across state-based exchanges.

Verification Required: Advanced Premium Tax Credits (APTC) are subject to reconciliation on your federal tax return. Consult a CPA regarding the tax implications of income projection methodologies. Always review the complete “Summary of Benefits and Coverage” (SBC) document before enrollment execution. “Short-term plans” operate under state-specific regulatory frameworks that vary significantly by jurisdiction.