Statute of Limitations on Medical Debt by State: What You Should Know

Empathy Hook

Receiving collection calls or letters about old medical bills can trigger real fear. You may wonder if you’ll be sued, if your credit will be destroyed, or if this debt will follow you forever. These feelings are valid, and you deserve clarity about your rights and options.

Understanding the Statute of Limitations (SOL) in your state is your shield. It determines whether a collector can legally force you to pay through a lawsuit. This guide will help you regain control.

When This Becomes Urgent (Legal Triage)

Most medical debt situations do not require emergency action, but certain legal signs demand immediate attention.

🚨 Act Immediately If…

- Court Summons: You received official papers for a lawsuit.

- Wage Garnishment: Threat to take money from your paycheck (requires a court judgment).

- Bank Levy: Threat to freeze your account.

✅ Take Your Time If…

- Just a Letter: Standard collection notice.

- Phone Calls: Annoying, but not a lawsuit.

- Very Old Debt: Debt is older than 7 years (Check your credit report).

The “Zombie Debt” Trap

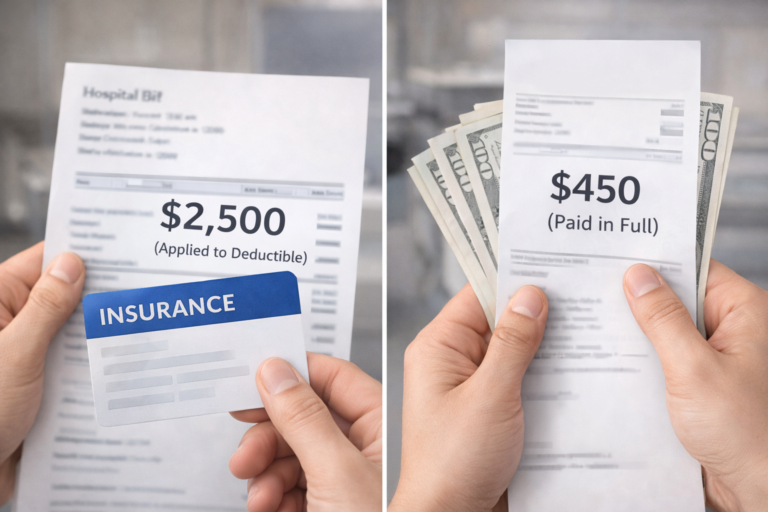

Medical bills range from small clinic visits to thousands for ER care. But the most dangerous part isn’t the amount—it’s the timeline.

⚠️ WARNING: Don’t Reset the Clock!

This is the #1 mistake people make. In many states, doing any of the following can restart the Statute of Limitations, giving collectors brand new years to sue you:

- ❌ Making a partial payment (even $5).

- ❌ Acknowledging the debt is yours over the phone.

- ❌ Agreeing to a payment plan.

👉 Rule of Thumb: Don’t pay a cent until you verify the debt’s age.

Timeline Reality Check

Understanding the difference between “Legal Time” and “Credit Report Time” is crucial.

-

⚖️ Statute of Limitations (SOL):

3 to 10 Years (Varies by State)

This is how long they have to sue you. Once this passes, the debt is “Time-Barred.” They can’t win in court, but they can still call you. -

📉 Credit Reporting Limit:

7 Years (Federal Law)

This is how long the debt stays on your credit report. After 7 years, it must fall off, even if unpaid.

What to Do Right Now

Take these steps to understand your situation and protect your rights. Acting methodically reduces stress and prevents costly mistakes.

🛡️ 3-Step Defense Strategy

- Don’t Talk, Write: Tell collectors to communicate only in writing. This prevents you from accidentally admitting guilt over the phone.

- Validate the Debt: Send a “Debt Validation Letter” within 30 days of first contact. Ask for proof of the original creditor and the date of service.

- Check Your State’s Law: Google “Statute of Limitations on written contracts in [Your State]”. If the debt is older than that number, send a “Cease and Desist” letter stating the debt is time-barred.

Strategy Showdown

🛑 Response Strategy Showdown

How to handle old medical debt

Navigator Alex Tip

What stood out was how often people unknowingly restart the statute of limitations by making even a small payment on old debt. Before you pay anything, verify the debt’s age and your state’s statute of limitations.

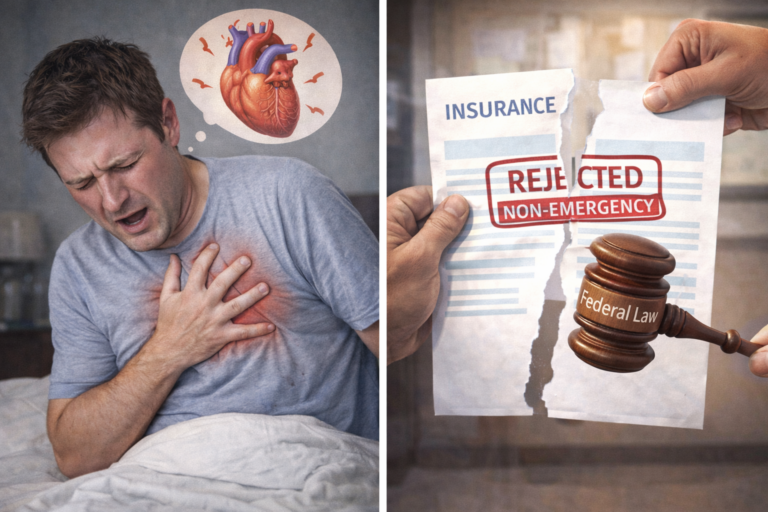

Pro Tip: If a collector threatens to sue you for a debt that is clearly past the statute of limitations, they may be violating the FDCPA (Fair Debt Collection Practices Act). You can report them to the CFPB.

Legal Disclaimer

Important: This article is for educational purposes only and does not constitute legal or financial advice. Statutes of limitations vary by state and specific circumstances. It is not a substitute for professional consultation with an attorney or financial advisor. If you are facing legal action or need specific guidance about your medical debt, seek immediate assistance from a qualified legal professional or consumer protection agency.